By MICHAEL FLITTON

The microchip industry is a case study in globalisation.

The US represents an enviable 38% of industry value but its participation is heavily skewed to upstream areas including core intellectual property research, design, and equipment. Asia meanwhile dominates the capital-intensive parts of the supply chain, including fabrication. This dynamic results from the necessary specialisation needed for the industry to successfully prosecute ‘Moore’s Law’, the prediction of relentless improvements in chip power, made by Gordon Moore, a co-founder of Fairchild and later Intel.

Rising manufacturing complexity creates a further winnowing of participants at each successive technological generation, or node. The foundational concept in classical economics is diminishing returns as supernormal profits are competed away. However, advanced technology, like microchips, exhibits characteristics of complex adaptive systems. Progress appears governed by increasing returns. The strong get stronger.

Chip fabrication is an extreme case in point. Here, the greatest yield learning gains within the industry are possible. The more chips you make, the higher your yields are. Efficiencies and experience gained can then be shared with future customers generating powerful network effects. Today, TSMC manufactures three times the number of semiconductors as Intel1 in its role as the world’s foundry.

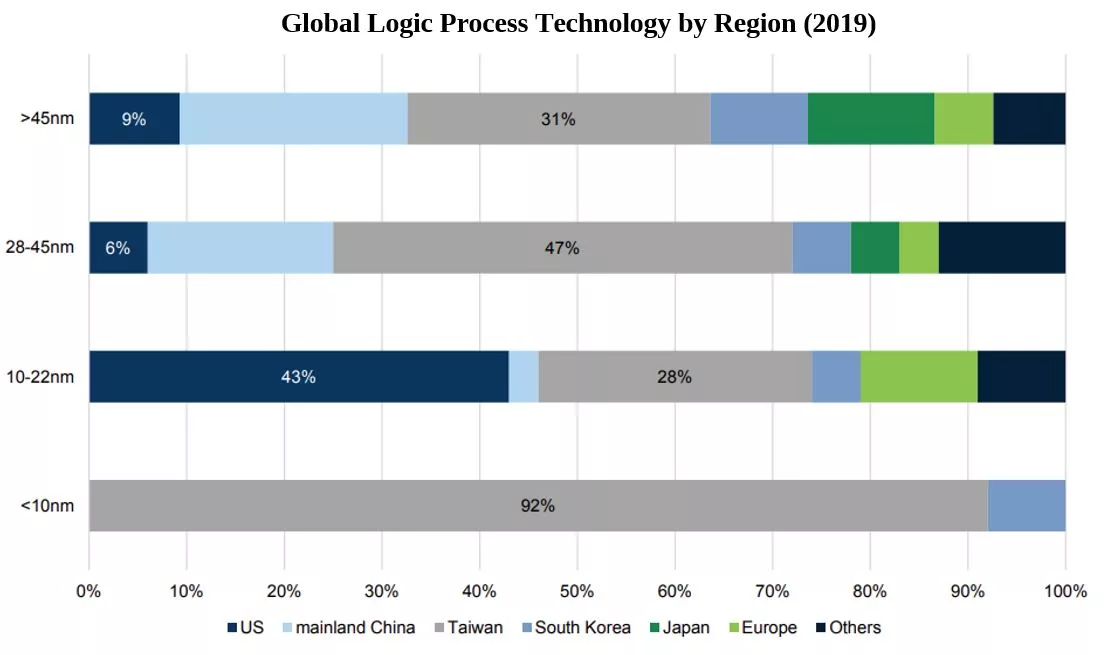

The effects of this flywheel are most evident at the leading nodes. For the most advanced chips the world relies wholly on the expertise of two countries, South Korea and more importantly Taiwan.

Source: GS

Source: GS

This skew has been implicitly accepted under the American led global order that has prevailed since World War II. It did not matter where the most advanced chips were manufactured given the alignment of national politics and interests. Now China has emerged as a vocal non-adopter of the US led system. Given Artificial Intelligence (AI) has been identified by both the US and China as the basis for military supremacy the concentration of advanced chip production in Taiwan matters. Hence, we have the CHIPS Act in the US, dual circulation in China, and even funding in Europe. However, in our view, it will be hard to displace the industry leaders.

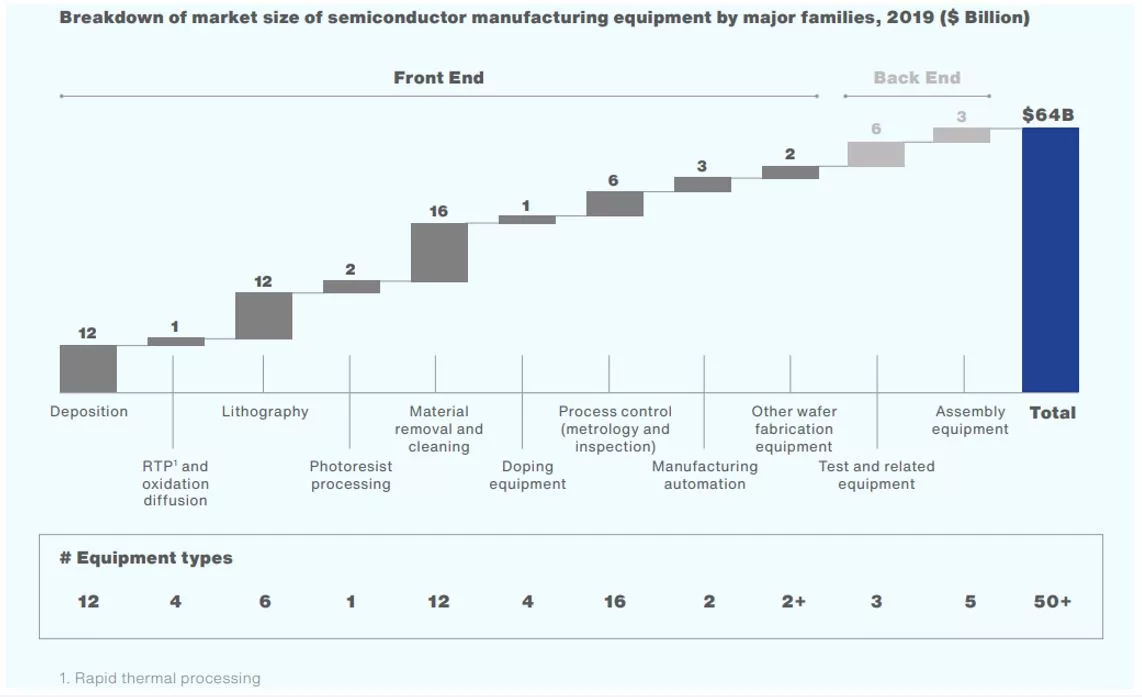

To compete successfully at the technological edge requires three core capabilities: equipment, know-how, and funding. Neither China nor the US has all three. The need for access to equipment is clear from this graphic. Fifty different advanced machines, each calibrated to the leading node, are needed to fabricate each chip. The US has this access, China does not.

Source: Gartner

Source: Gartner

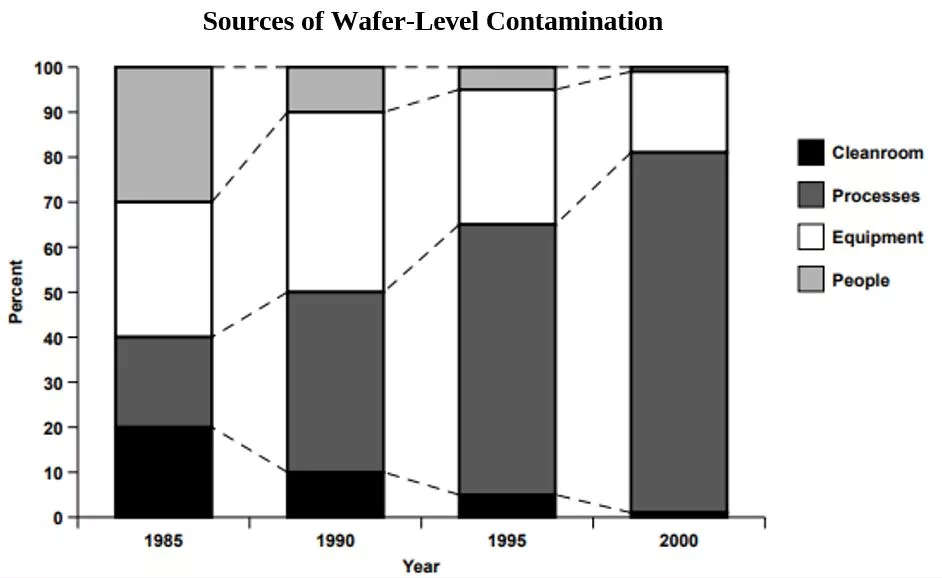

You can have the equipment but without the process you are stuck. A recipe is needed to make a cake. The importance of the recipe is shown here with a slightly dated graphic. It highlights how process has come to define success.

Source: IC Engineering

Source: IC Engineering

This results from the extreme complexity of chip manufacturing. Iteratively perfecting the process, yield learning, is the heart of the IP in foundry. This is an intangible asset, which cannot easily be ported without taking the whole engineering body. This is where Intel has fallen behind and catching up will be hard. For China, the task of overhauling its deficit to the cutting edge is more significant and will likely require the acquisition of know-how. China has been engaged in a broad-based hiring of high-skilled engineers from leading companies for some time to achieve this end. It is telling that the US has targeted access to US talent in its latest sanctions against China. Without the people there is no hope of securing the process.

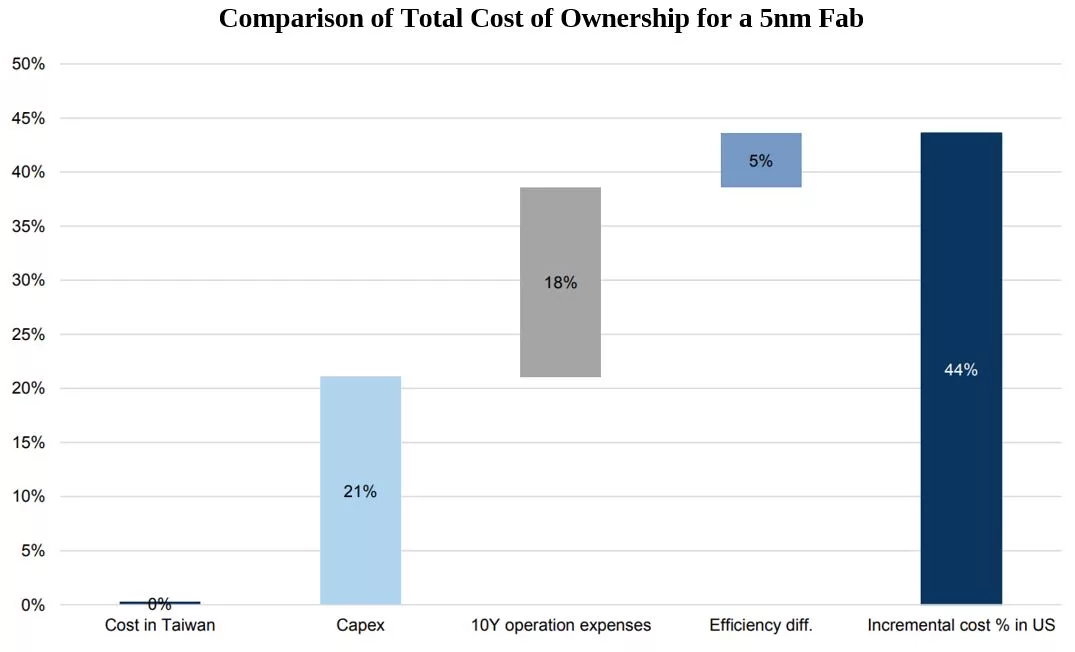

Finally, fabs cost a lot of money. China’s centralised system allows it deep pockets. The US is largely a private sector structure and so government funding has historically been limited. Goldman Sachs analysis, shown below, corroborates Morris Chang’s estimate that a cutting edge fab would cost 40%-50% more over its lifetime in the US compared to Taiwan. To incentivise capital allocation to the US the government will need to fund the difference to the private sector. That would be billions per fab per year. This is feasible in the current climate but may be less politically palatable over the long term.

Source: GS

Source: GS

Despite government rhetoric from both sides the current industry structure will be hard to disband, in our view. The scale of the political will should not be underestimated but neither should the strength of the existing flywheel. The future is uncertain however, we can surmise that the current manufacturing concentration in Asia is unlikely to be sustained at current levels ten years from now.

We remain flexible in our thinking around probable outcomes but we believe this scenario still leaves ample room for the companies we own to be successful. We note valuations are compelling after the decline in sentiment this year. Across Cerno Global Leaders and Cerno Pacific we own critical businesses with large market shares in niches of the supply chain with a bias towards advanced equipment manufacturers.

1Chip War by Chris Miller